Rental Survey 2015

29/10/2015

Click here to download the complete PDF

Background

Over the past 12 months both the UK and global economies have seen an improvement following the pressures created by the banking crisis and the wider worldwide economic downturn. Banks, perhaps under central government encouragement, continue to ease their strict loan criteria. UK interest rates and inflation remain low together with falling unemployment provide a solid base from which the economy can grow. Whilst market conditions have generally improved within the UK, there continues to be international pressures. This is in part due to the uncertainties within the Eurozone. More recently we have seen the slow down in the growth from the emerging nations; particularly the likes of China and India.

The UK has always benefitted from a high level of overseas investment, particularly in the property market, which has always been considered a safe haven. This investment continues at unprecedented levels. Low returns from savings has lead to people seeking alternative investment vehicles, including licensed and leisure properties, which offer good returns. This investment has been particularly noticeable within the London property market. More recently we are seeing this starting to spread to the regions.

Brasshouse, Birmingham

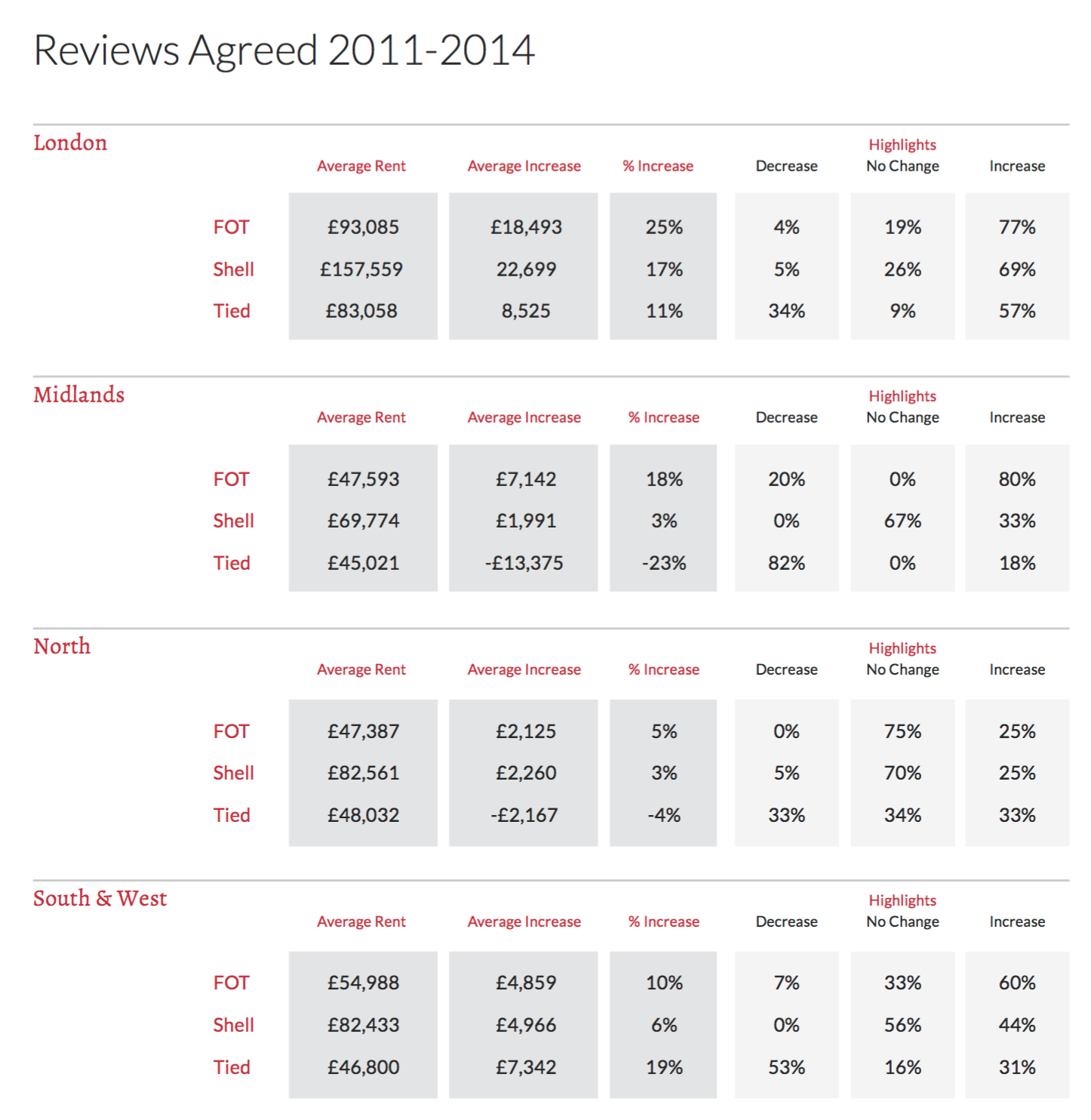

London

The London market continues to dominate as the largest single area of activity. Many more lease renewals and rent reviews have been concluded in London than throughout the rest of the UK. This is in part down to the buoyant market that has been experienced over the past 3 years. This is in sharp contrast to the rest of the country, particularly the northern regions.

With the booming economy within the M25 operators have been keen to secure sites to maximise the benefits of the increased leisure spend. With only a limited amount of operating space being available and an increase in demand, which has outstripped supply, rents as a consequence have been forced upwards. New entrants to the market are also creating a surge in rents, particularly within the restaurant sector.

One of the biggest drivers to the London market has been the significant increase in overseas investment, as referred to above. This coupled with occupier demand has pushed property prices to record levels. With the increasing property prices investors are, not surprisingly, keen to see return on their investment. This has resulted in many more rent reviews being actioned.

Major areas of activity have included the West End, Soho and Covent Garden. In addition, areas that were once considered to be secondary locations are starting to attract mainstream corporate interest. These areas include districts such as Shoreditch, Stoke Newington, Hackney and Brixton.

A further consequence of London's growth is that many operators are starting to see a squeeze in returns due to higher overheads, particularly rents. This has forced many to seek outlets in less pressured areas on the outskirts of the city. In addition many London operators are now seeking representation in the wider UK market.

When considering any statistics it is no surprise that London rents are significantly higher than the rest of the UK. Of particular note are levels of shell rents within central London, which have an average rent of £151,000 per annum. This is underpinned by some significant rents in prime locations, which have, in a number of cases, been well into the hundreds of thousands of pounds per annum. In fact, the highest rent we have seen has been in excess of one millionpounds per annum. Growth within London appears to be unabated, although as with any cycle, this cannot continue indefinitely. The difficulty is predicting when this level of growth will slow down.

Piccadilly Institute, London

Regionally

Apart from London, the rest of the UK has seen significant variations. Some of the urban centres, particularly the likes of Manchester, have witnessed increased rents, particularly in prime areas such as Spinningfields. A similar situation has been witnessed in Liverpool, with the Liverpool One scheme.

One common theme identified in the regions has been London operators seeking representation outside the capital. We have seen regional shell rents in some areas being pushed to figures well in excess of £40 psf. Whilst this level of rent may appear cheap in comparison to prime rents within central London, this is still a significant increase over historic levels. These rents may ultimately be at a level that are unsustainable in the long term.

As has been voiced elsewhere there are concerns of London operators coming into the regions, opening up new outlets at high rents and ultimately failing because their offer did not work outside London. This has left the legacy of high rental evidence, which astute landlord's surveyors are utilising to force rents up to levels that are not sustainable. This may only be a short term benefit to any landlord. More failures may result in empty units that may prove difficult to re-let and ultimately have a negative impact on rental values.

Landlords are also heavily incentivising tenants by way of reverse premiums, contributions towards fit-outs, extended rent free periods etc. These transactions may not always be transparent and may create problems for the unwary surveyor. It is essential to know the full details of any new letting. These deals also put into doubt the old adage that new lettings are the best evidence.

Garrick, Stratford On Avon

Restaurants

This is one area of the leisure market that has seen the most significant levels of activity. The growth in dining out appears to be unabated. Corporate restaurants continue to be one of the main driving forces in new openings, with many new leisure schemes having new units taken up as pre-lets.

Whilst many restaurateurs continue to increase their estates, this activity has not been restricted to London markets. Many restaurateurs are now seeking representation outside London. These operators include the likes of Byron Burger, 5 Guys, Burger & Lobster, Darwin & Wallace and Côte. Other branded operators such as Nandos, Chiquitos and Frankie and Benny's continue to expand, as do operators such as the Tim Bacon backed, New World Trading Company.

In addition, many restaurateurs are developing their offers within traditional public houses rather than converted high street retail units or out of town leisure parks. With dining out nowbeing an everyday part of the UK lifestyle, this element of the leisure market is likely to continue to grow for the foreseeable future. If, however, once saturation point is reached there is likely to be a slow down in rental growth.

Pubs

Both Free of Tie and Tied pubs have seen varied results. Many of the Pubcos and brewers now operate within industry approved Code of Practise schemes. This assists tenants in providing an understanding of the process that the landlord will go through when actioning arent review. Landlords are required to be far more transparent than they have been historically. These new regulations, which have created a level playing field between landlords and tenants, now allow tenants to obtain rent reductions where the situation permits. Over the forthcoming review period we should see a balancing of rents that will become affordable. It should be remembered that it is only those pubs held on tied leases that benefit from the Codes of Practice. Free of Tie pubs continue to be held on standard commercial leases.

The statistics show that a number of areas have seen decreased Tied pub rents. London had 44% of rent reviews seeing a decrease, the Midlands 82%, North 33%, South and West 53%. This will be primarily as a result of the Code of Practise allowing rents to go down, which had not previously been the case. It may also be that these statistics reflect the fact that Fleurets have only been instructed to undertake a risk assessment where there may be a potentialproblem. Thus these reviews may not be representative of the wider tied trade market.

Tied rent averages throughout the regions also show a degree of consistency, being between £45,000 and £48,000 per annum. Again, this is possibly higher than the national average and may reflect the involvement that Fleurets have been active at properties where high historic rents have been challenged.

Many tied lease operators are continuing to support their tenants by other means, including rent abatement and increase in the level of wholesale discounts to the tenants. As with any rent review either shell letting on the high street or a tied lease, the rent payable has to be affordable by the tenant.

Free of Tie rents generally are seeing an increase. The main areas of growth have been in London and the Midlands. This may be a reflection of the greater demand combined with a more restricted supply forcing an increase in rents. In addition most free of tie leases will have upward only rent review provisions, thus rent reductions are less frequent.

Perhaps the biggest issue facing the pub market is the forthcoming Market Rent Option (MRO), which is likely to come into effect in the next 12-18 months. There have been many suggested outcomes to this. We have seen exclusively tied lease operators start to set up managed house divisions as a forerunner to avoiding the impact of MRO. Tied tenants need to be properly advised as this is not just a case of moving from tied to free of tie status without any impact on rent. All things being equal rents will inevitably rise by going free of tie. Landlord

companies have also been reluctant to grant longer leases, thus reducing the potentialassignment value to the tenants. Also as SCORFA benefits erode running costs are likely to increase. As with any change in legislation there is the potential for unintended consequences. A feature of the proposed legislation, as with the Beer Orders is the possibility of unintended consequences.

The most significant issue in this respect going forward will be levels of beer discount rates. MRO and resulting free of tie rents will flow from prevailing levels of discount, which presently are at an all time high, resulting from large scale purchasing power and a demand base in persistent long term decline. It seems very likely the large scale brewers would welcome an opportunity to recover some ground on their pricing. Any further consolidation in the brewing sector could lead to greater price control, hence driving down discount levels. In this respect though there may be some differences in the pricing dynamics for the large Pubcos that also brew their own products, such as yourselves, Marstons and Star Pubs/Heineken as compared with Admiral, Enterprise Inns and Punch Taverns.

The MRO approach will substantially pass the discount rate risk to lessees and tenants, and any fragmentation of the purchaser market will strengthen the position of the major brewers. Falling levels of discount would increase the risk of higher fixed costs, potentially raise retail prices and reduce long term investment, therefore exacerbating the situation. A relatedunintended consequence may be that in such circumstances operators would react by concentrating their range of purchases, in order to maximise discounts, hence reducing consumer choice.

Shell Lettings

Free of Tie leases are not subject to the industry Codes of Practise and not surprisingly the majority of these leases have seen no change or an increase. Similarly, shell lettings, which are held on standard commercial leases with upward only rent reviews, also show limited numbers where rents have decreased. These have generally been re-lettings of existing units, where the new tenant has been able to secure, what may have been a previously failed unit, for a lower rent than had previously been agreed.

Not surprisingly average rents for all sectors are highest within London. In the regions, free of tie rents are relatively consistent, although the South & West show a slightly higher average rent than the North and Midlands. Average shell rents within the North and South & West are identical. This may reflect that many of the shell rents dealt with have been in prime locations where there is a degree of consistency with corporate operators achieving similar trading levels.

The high street market continues to evolve. In many urban centres new circuits are being created. The consequence of this is that many units once considered in prime locations now find themselves off pitch and possibly over-rented. This is an inevitable feature of urban development which will continue as more investment takes place. Again it is a surveyor's local knowledge of market that is key to getting the best deal. Going forward we still anticipate more consolidation within the high street sector. Only recently we have seen with the acquisition of the TCG estate by Stonegate.

Conclusion

As with any statistics, it is the background information relating to these figures that gives a greater understanding of the final figures. It is essential that statistics are not relied on in isolation and parties should obtain professional advice to ensure that the appropriate market rent is negotiated. It is anticipated that with the improving economic conditions and the push ofoperators outside London there to be a general improvement in rental values over the coming years, although this will only impact as and when rent reviews or lease renewals fall.

Whilst the effects of the recession begin to wain we still have various austerity policies in place. Interest rates remain low and there are still no signs of a rise any time soon. Leisure property continues to attract investors and with an increase in leisure spending the licensed and leisure market will continue to grow. With this growth we are starting to see more rent reviews being actioned. This trend is likely to continue over the coming years, though inevitably there will be some winners and some losers. To ensure the correct outcome is achieved it is always best to ensure you have sound professional advice from surveyors who understand the licensed and leisure sector.

White Lion, Barthomley

White Lion, Barthomley