On Market

03/12/2018

Click here to view the online magazine.

Click here to open the pdf directly.

A comprehensive review magazine with topical articles from Fleurets' experienced staff, alongside a taster of completed transactions, current instructions and professional advisory work.

In this issue:

Should I stay or should I go?

Phil Smith guides you through the process of renewing a commercial lease.

Thriving in uncertainty

Director and Head of Hotels, Paul Hardwick, analyses the latest UK hotel data.

Make hay whilst the sun shines

Rosie Hallam looks at strong Net Initial Yields in these uncertain times.

A taste of success

Richard Thomas explores some of the thriving businesses in a turbulent restaurant market.

Pub Sales- A multi layered market

Director of Agency, Simon Hall, looks at pub transaction volume across the North.

Live & let live

Kevin Conibear takes a look at the evolution of the music industry across the UK.

A kick of caffeine

Much like 1976, 2018 will live long in the memory and be referred to over the years and decades ahead during weather forecasts and climate change documentaries. Although the trading performance of wet-focussed pub operators may not last quite so long in people's memories, the performance of JD Wetherspoon, Stonegate and the vast majority of traditional tied pub tenants across the country should not go unrecognised. JD Wetherspoon delivered 5.5% like-for-like sales growth (LfL) over the 13 weeks to 28th October, whilst Stonegate delivered 4.6% LfL over the 40 weeks to 1st July. Similarly, Ei Group reported net income growth of 1.3% over the 47 weeks to 25th August, it being quite clear that the warm weather drove us all to quench our thirst in pub beer gardens across the country.

The warm weather coincided with the FIFA Football World Cup which provided a trading bonanza for sports focussed venues. Stonegate achieved LfL growth of 19.2% during the World Cup, with 4.5 million pints sold during the tournament. Personally, I am not sure that England's achievements at the World Cup were that notable, a record of played 7, won 3, lost 3, drew 1, would only amount to mid-table obscurity, but that debate is for another day. It is clear that all wet-led pub operators should give Gareth Southgate one on the house should he pop in!

Whilst the executives of the wet-focussed pub operators have been collectively patting themselves on the back, their counterparts over in the casual dining sector will have been fervently playing with their worry beads and asking whether 2018 can get any worse. The last thing that the likes of Prezzo and Carluccio's would have wanted is a record breaking summer.

However, it remains unclear as to whether the worst is over for this sector of the leisure property market. The issues of rising costs in relation to food supplies, business rates, rent and labour remains as prevalent now as they did 12 months ago. The issue of labour supply is likely to become the most concerning of these issues in the year ahead as net migration to the UK from other EU countries continues to fall. As a result, this may lead to wage growth as operators throughout the leisure sector find securing good quality candidates more challenging.

The property market itself has experienced a comparatively buoyant and healthy period, with notable transactions across the pub, restaurant and hotel sectors; The Restaurant Group (TRG) being particularly active, picking up Food and Fuel (11 leaseholds in London) for £14.9m, quickly followed by the agreement to purchase Wagamama (133 restaurants in the UK, plus 63 worldwide) for £357m in cash, in addition to the existing debt of £202m. The acquisition of Costa by Coca Cola, however, stole most of the headlines and numerous column inches. Whether the deal means we will see Costa explode across the globe is unclear, but a more direct consequence is likely to be further investment and growth of Premier Inn as Whitbread use some of the disposal proceeds towards accelerating investment in the hotel brand.

The months and year ahead is likely to be both challenging and exciting for leisure property owners and operators alike but, as ever, I am optimistic that the conditions are right in the sector for success.

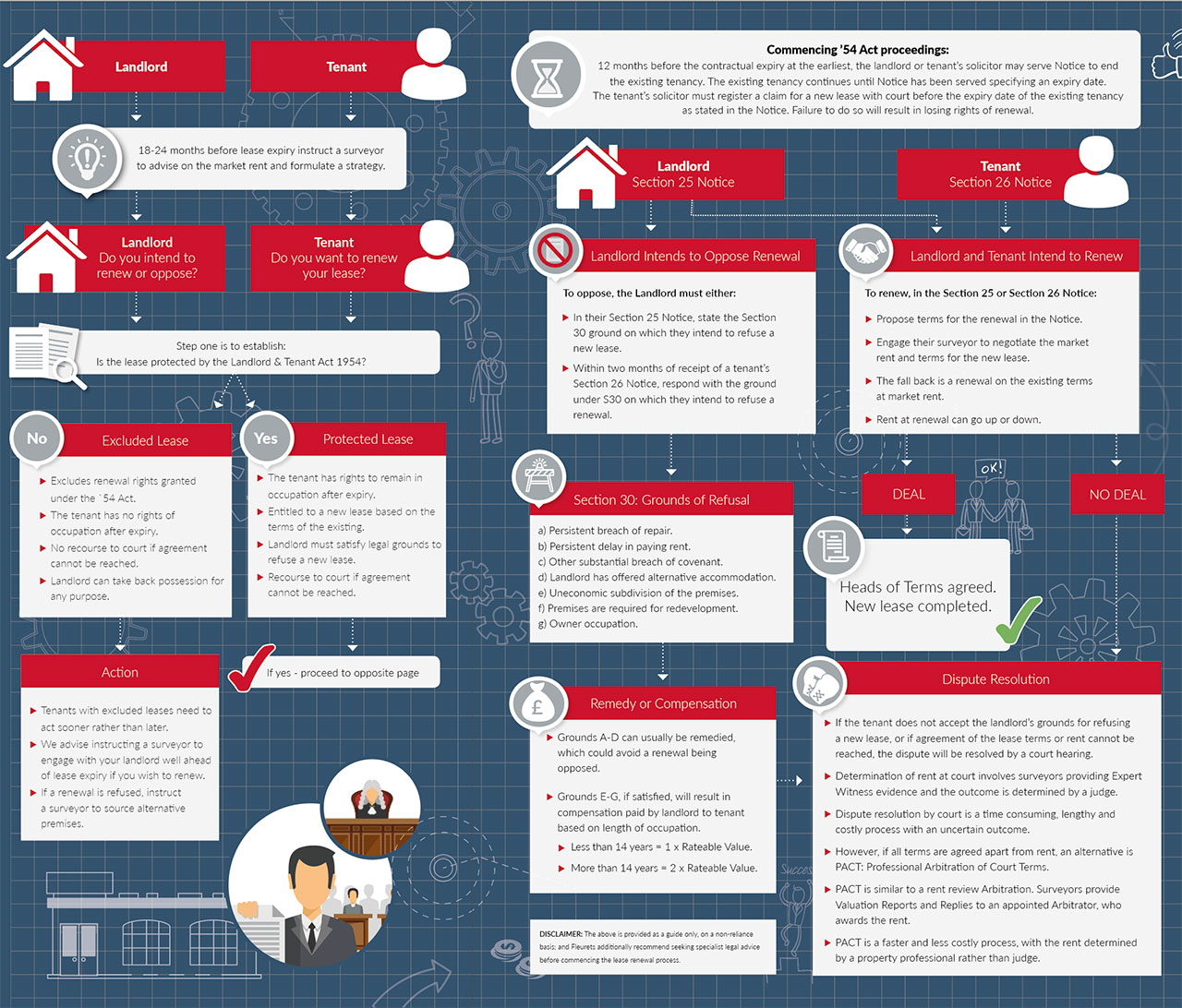

Should I stay or should I go?

Philip Smith - Divisional Director

Facing a lease expiry can be a daunting prospect with an uncertain outcome.

Philip Smith, specialist in Lease Consultancy, guides both landlord and occupier through the process of renewing or refusing a renewal of a commercial lease, under the Landlord & Tenant Act 1954.

As this process map demonstrates, the lease renewal process under the `54 Act is complicated. Involvement of courts, solicitors and surveyors may seem daunting but, nevertheless, with the landlord and tenant aiming to secure the future use of the property, it is a pivotal event in a property's life cycle and it is vital to be on top of the process.

As ever, it pays to take early advice; Fleurets' nationwide team of Lease Consultancy professionals have the expertise to guide you through the process from start to finish.

DISCLAIMER: The above is provided as a guide only, on a non-reliance basis; and Fleurets additionally recommend seeking specialist legal advice before commencing the lease renewal process.

DISCLAIMER: The above is provided as a guide only, on a non-reliance basis; and Fleurets additionally recommend seeking specialist legal advice before commencing the lease renewal process.

Thriving in uncertainty

Paul Hardwick - Director & Head of Hotels

Following a strong second half, 2017 transaction volumes in the hotel sector reached circa £5billion, a significant leap from the previous year, driven by a significant number of Central London trophy hotel sales in the first half of the year followed by a number of large portfolio transactions in the second half. This continued into 2018 with further portfolio transactions dominating the first half of the year, including the sale of the remaining Amaris Hospitality Hotel Portfolio for circa £600million, Apollo disposed of its 20 unit Ribbon Hotel portfolio for c.£742m and Starwood Capital exited from the 14 unit Principal Hotel Portfolio for c.£830m. With a number of additional transactions in play, anticipated to complete prior to the end of the year, 2018 looks like it will be ahead of last year by a significant margin, albeit with a much lower contribution from single asset transactions.

![]()

The market is experiencing a shift in buyer profile with European and Middle Eastern investors, alongside real estate funds, family offices, small and expanding multiple operators and other longer term investors coming to the fore.

Particularly strong appetite exists for investors looking to secure long dated, fixed income assets, hotels as an alternative investment class being very much in the sights, an example of which being Secure Income REITS' acquisition of 76 Travelodge Hotels for around £245million earlier in the year. Investments with index linked growth prospects are attracting very keen yields, Premier Inn Hotels and Travelodge investments frequently transacting.

We are also witnessing the growing occurrence of ground lease/income strips as an alternative method of financing with hotel owners/buyers capitalising on the weight of money chasing long term secure income investments, confident that the value of their retained long leasehold hotel interests are supported by the strong prevailing hotel market conditions.

There also remains a steady flow of selective purchases by both established and expanding multiple hotel operators.

- Earlier in the year Fleurets acquired two Surrey hotels on behalf of Young's - the 43 bedroom Park hotel, Teddington and the 51 bedroom Bridge Hotel, Chertsey, for around £11.6m.

- Acting on behalf of the Coaching Inn Group, we acquired the group's 15th hotel, the 31 bedroom Swan Hotel in Stafford, from the Lewis Partnership.

- We very recently concluded the sale of the 60 bedroom Manhatten Hotel in Blackpool to Daishs Travel off a guide price of £895,000, increasing their portfolio to nine hotels.

With continued uncertainty around Brexit, a large proportion of hotels now owned or having been acquired by longer term investors, transaction volumes over the coming year are expected to be more subdued, perhaps more aligned to 2017 levels.

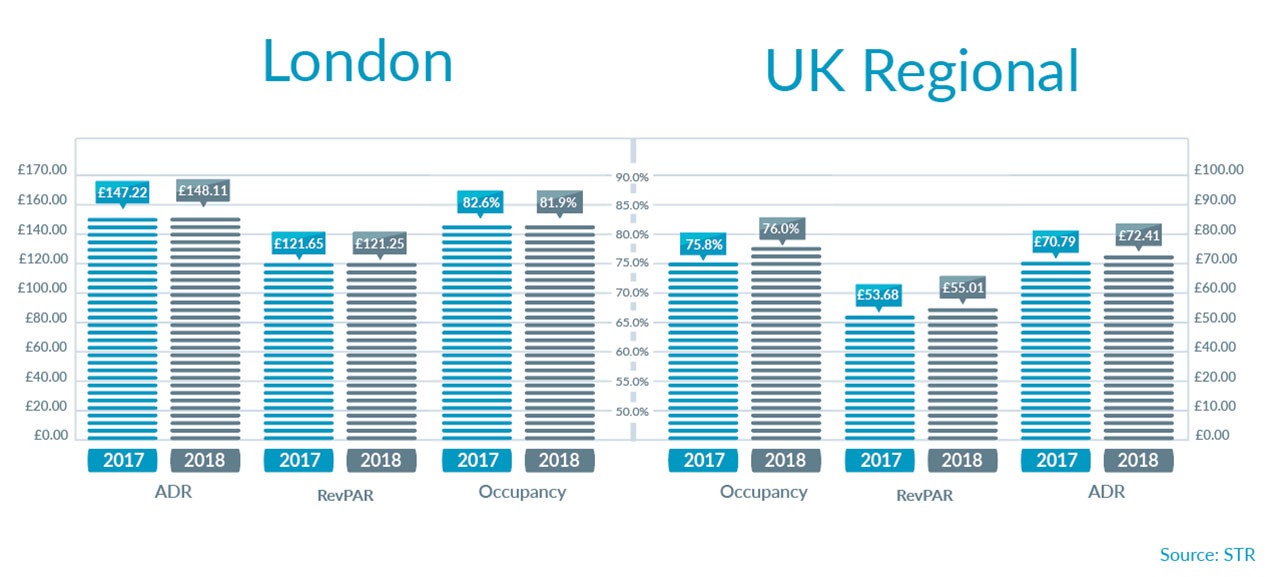

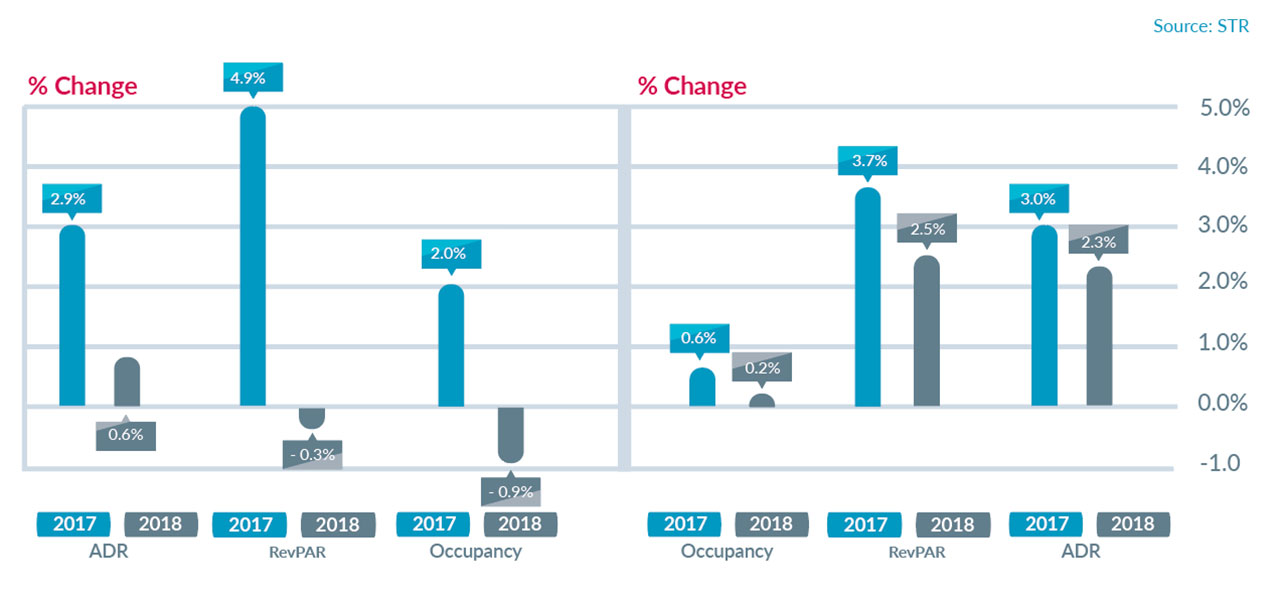

Hotel trading performance across the UK remains robust. London hotels continue to perform at very high levels, albeit having somewhat plateaued, and the regions continue to demonstrate solid growth.

![]()

Key performance statistics reported by STR on a 12 month moving average basis for the two years to July 2018 are summarised below.

In the case of London, the 4.9% RevPAR growth to July 2017 has not been matched this year, and although hotels continue to benefit from a strong leisure market aligned to the weak pound and buoyed by a number of key events, hotels face challenges from economic uncertainty, significant increase in hotel supply and suppressed business demand.

Expectations are that London is likely to continue with largely flat performance, with forecasters anticipating a potential small decline next year, primarily as a result of occupancy levels slipping.

Regionally, hotel occupancy has been relatively consistent during the last few years. Current levels are enabling hotels to continue to drive ADR, the 12 months to July 18 reflecting 2.3% growth on the previous year, driving 2.5% growth in terms of RevPAR. Further growth, albeit more subdued, is anticipated.

New hotel and room supply remains a dominant disrupter within the region of 10,000 new rooms expected to enter the supply chain in London and approaching 15,000 regionally over the next year or two.

Ten years ago, around the prerecession market peaks, it was common for hotel purchasers to pay prices that included material hope value to reflect the untapped management opportunity and investment potential.

In the current marketplace, buyers and their valuers are more cautious, reflecting market driven opportunity in pricing, whilst not underestimating risk. Buyers are being more selective, applying a greater degree of due diligence in their appraisals.

Source: STR

Source: STR

Whilst hotel pricing within prime Central London might reflect trading income yields around 5% in some instances (profit multiples in excess of 20 times), pricing levels are often skewed by perceived underlying real estate values (e.g. residential).

Regional pricing is much more closely aligned to traditional income considerations and return on capital requirements, yields often typically fall between 8.5% and 12.0% (multiples of c.8 times to 12 times).

Higher prices reflect those businesses that are in good condition, well operated, require minimum capital investment and are available with a supporting proven history of successful past trade and profit performance. These businesses offer buyers and funders greater confidence, and are most likely to receive maximum interest with the opportunity for competitive bidding.

Key to a fluid transaction market is confidence; in terms of economic conditions; consumers supporting hotel trading performance through leisure and business spending; visitors and their security whilst in the UK; operators and buyers in terms of formulating business projections, investment plans and considering expansion opportunities; funders and their credit teams measuring ongoing support and acquisition lending; and sellers aspiring to maximise exit proceeds.

Mounting Brexit uncertainty is certainly doing no favours for confidence, however, some might say that this presents an exciting opportunity, and so far at least, the hotel sector continues to thrive.

The Old Red Lion, Holborn

The Old Red Lion, Holborn

Make hay whilst the sun shines

Rosie Hallam - Senior Associate

Granted, the first half of 2018 has hardly been pleasant for high street retailers and casual dining operators, but, as with the weather, and so many other things in life, it is likely to be just a phase! For several years there has been strong private equity investment into the casual dining sector, with new brands being rolled out across the UK, seeking to satisfy our apparent insatiable hunger for more. It was perhaps inevitable, however, that there would be some casualties.

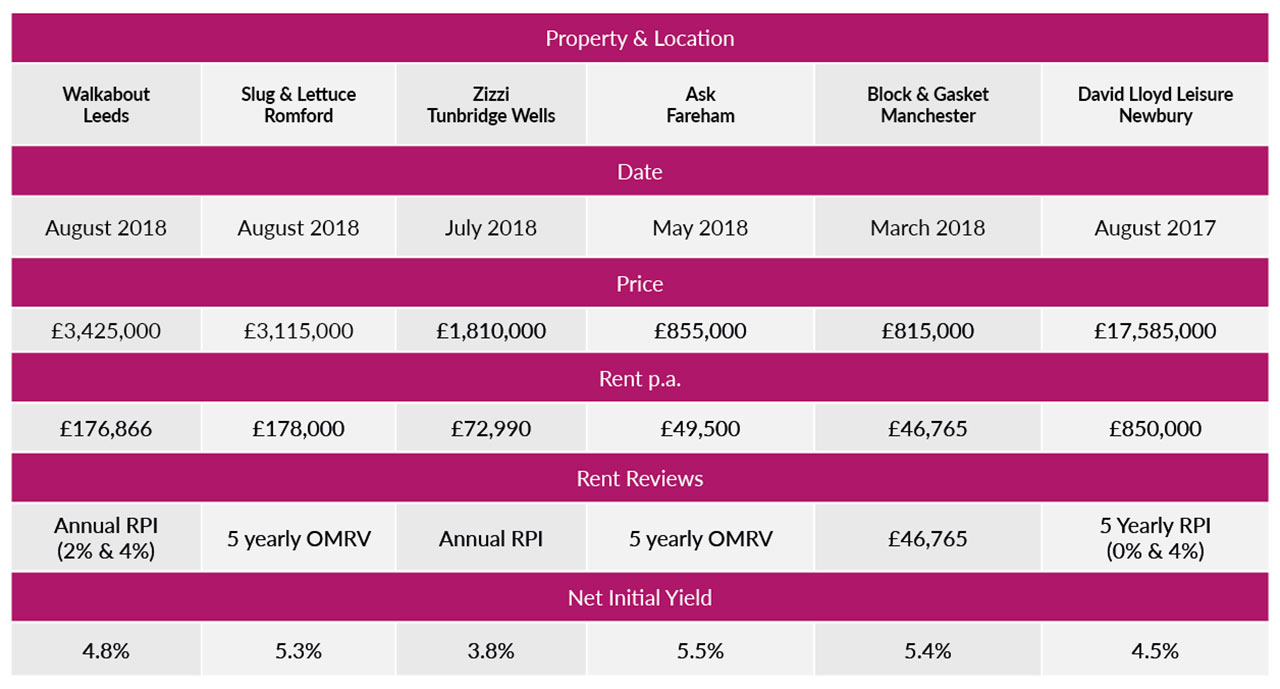

However, the challenges of the casual dining market have not diluted investor appetite as underlying fundamentals within the leisure property market remain strong, with keen yields being achieved across the country for the best assets and opportunities, as the table illustrates.

Leases with long unexpired lease terms, robust covenant tenants and annual index linked rental increases remain the key criteria, characteristics that are commonly seen in the public house sector, and investors are keener than ever to tap into this sector of the market place.

Increased like-for-like sales have been reported across a number of the major pub companies, including Fuller's, Young's, City Pub Company, Mitchells and Butler and Stonegate, and the likes of Ei Group Plc have reported growth in net income.

With a trip to the pub proving more attractive than ever, especially with the boost from the 2018 World Cup and summer heat wave, strong rental growth, especially across the south east, and low interest rates fuelling cheap finance, the attraction of the pub sector for property investment has proven increasingly difficult to match.

Fleurets is active in the leisure property investment market place acting for investors, operators and individuals alike, advising on acquiring and disposing of such assets.

Earlier this year Fleurets sold the Walkabout, Leeds, operated by Stonegate, in an off-market transaction for £3,425,000 reflecting a NIY of 4.85%. Fleurets has also recently acquired Riverside House in Bristol on behalf of City Pub Company, who were the tenants in situ, for a sum of £2,100,000, reflecting a NIY of 4.26%, thus demonstrating the demand for key sites and securing long term security over their occupation.

Our agency team has recently brought to the market two highly attractive, central London, tied public house investments, the Red Lion in Holborn and Queen's Larder in Bloomsbury, with guide prices of £2,150,000 and £2,250,000 respectively. This follows the recent sale (subject to contract) of the Tollington Arms in Hornsey, off a guide price of £2,200,000, also let on a tied lease.

In addition to our activity in buying and selling leisure property investments, Fleurets continue to be well-placed to provide valuation advice in relation to acquisitions and have advised a number of institutional investors in this regard.

We would be pleased to discuss your current investments and future investment requirements.

Net Initial Yield (NIY) stated after deducation of standard purchaser's costs

Net Initial Yield (NIY) stated after deducation of standard purchaser's costs

The Wolseley

A taste of success

Richard Thomas - Divisional Director

It is easy to look at the current restaurant climate and see closures as the 'death of the high street'. At Fleurets we challenge that vision and see every closure as an opportunity.

Desire to own a restaurant in the capital is relentless, and these developments in the sector are giving many emerging operators their chance to shine. For example in 2018 vegan pizza concept, Purezza, opened their first London site, in Camden, expanding to the capital from their Brighton home.

Similarly, earlier this year I was involved in a flagship acquisition of Hai Di Lao, Piccadilly Circus (formerly a museum) extending to 2,000 sq ft at ground floor and 8,000 sq ft in the basement,at a commencing rent of £1.25 million, equating to a weighted ground floor rate of £200psf, marking the operator's first site in Europe. They will now look to expand into other European cities as well as UK towns, with present discussions for a second site in East London.

Whilst the casual dining sector is somewhat in turmoil, new entrants are able to take advantage of the units being vacated.

In contrast to the casual dining sector, the high-end Central London restaurants have remained relatively stable and continue to flourish.

Corbin & King, the operator of six Central London sites, as well as, Café Wolseley in Bicester Village, illustrate this point perfectly.

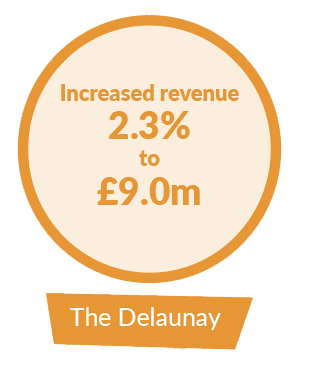

Irrespective of difficult economic times, not to mention a week's closure and subsequent disruptions at The Delaunay due to a close by fire for the year ending 26th March 2017, The Delaunay announced increases in revenue by 2.3% to £9.0m.

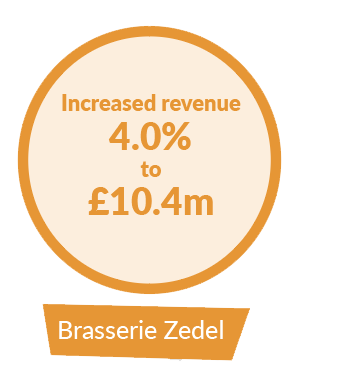

The Wolseley and Brasserie Zedel increased their revenue by 3.3% and 4.0% respectively over the same period.

Exemplary service, a distinctive offering, central accessible locations in combination with spectacular settings financially show their worth.

Corbin & King's company accounts, interestingly highlight the added benefit of group operations, being able to share the central services of procurement, personnel and training. Furthermore, the group also highlight staffing as a key ingredient in their recipe for success; 'workforce [is] its most important asset'.

Similar to the new entrants in the casual dining market, high end restaurants are also on the acquisition trail. For example, Petersham Nurseries expanded from their primary Richmond location into Central London.

Their Covent Garden site supplemented its deli/retail operation, adding two restaurants, set around an internal courtyard and spanning over 16,000 sq ft. The rental for this operation is circa £2,000,000 p.a. and opened in February 2018.

And expansion is not limited to London. D&D London, the group behind German Gymnasium, Le Point de la Tour and Skylon, to name a few, have recently reported strong financial resultsfor 2017/18, with a 6% increase in turnover to £132.2m. With a strong existing London portfolio, the group are broadening their reach, having recently opened 20 Stories in Manchester.

The benefit of high end, destination restaurants is that more often than not, it is the name of the chef or the sheer reputation of the quality of food, service and overall experience that drives trade, not whether is it located in an iconic or high footfall position, although it does help! Consequently, being in super prime central city locations is not always important. In fact, many such restaurants are in arguably slightly off pitch locations by comparison.

Notwithstanding this, demand remains strong, especially as operators seek these alternative locations in an effort to balance location with affordability, and rental growth is being seen across the board.

Fleurets is acting for the tenant, the renowned chef, Jason Atherton, in connection with the rent reviews of his Michelin starred restaurants, the Social Eating House on Poland Street, Soho, and Pollen Street Social on Pollen Street, Mayfair, seeking to secure the best outcome possible in an ever competitive market place.

Armed with just a small handful of examples I hope I have illustrated that the restaurant market (not the food!) is indeed alive and kicking, and opportunities continue to present themselves and be created.

Pub Sales - A multi layered market

Simon Hall - Director - Agency

Transactions in the pub market have always been dictated by the availability of finance, but the effect on deals has never been so diverse, especially in the north.

There is no shortage of buyers with plenty of cash or talented operators, however there are precious few who have both.

The combined effect is that there are several types of property that are in strong demand and others where demand is limited. Understanding the precise pockets of demand is critical to assigning value.

High demand exists for top end sites suitable for managed operation, city centre sites, bottom end freeholds, leisure investments and nil premium free of tie leaseholds.

There is less demand for mid-sized owner-operated businesses, which, despite being very profitable, solid operations, available at exceptional value, have fewer buyers because of the amount of cash down payment needed.

With deposit, fees, SDLT, stock and working capital this is often 50% of the purchase price.

The overall volume of transactions has remained steady across the north. Large managed pubs have sold well to regional brewers and developers alike. Pubs in city areas have sold to local multiple operators and many suburban operations for alternative use, including cafés, corner shops and for residential.

With values steadily increasing, Loan to Value rates stuck at 60% and continued uncertainty over Brexit, it doesn't appear this is set to change anytime soon.

![]()

Live & let live

Kevin Conibear - Head of Urban Markets

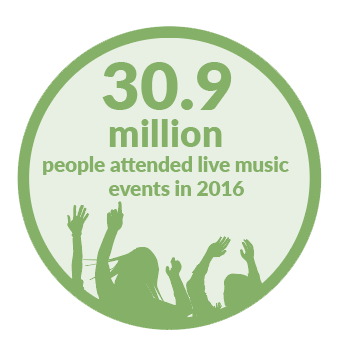

In 2017, music contributed £4.5bn in Gross Value Added (GVA) to the UK, up 8% over two years, according to UK Music's Measuring Music 2018 Report. Live music increased 14% in 2016 to make up almost £1bn of that figure and 30.9 million people attended live music events across the UK, a 12% increase on the previous year. The live industry supported 28,659 jobs in 2018. Deloitte reported that live performances such as concerts and theatre generated £2.1bn in 2017, with concert-going accounting for more than 50% and forecast 7% growth in 2018.

These headlines are positive, but there are some underlying challenges affecting operators,especially smaller venues that are the breeding grounds for emerging talent. Despite being in an age of TV talent shows and social media catapulting unknown artists to stardom, the majority of acts start from nowhere, performing in small independent venues, honing their talents, before hitting the mainstream. The likes of Coldplay and Ed Sheeran began here, before they hit the iconic status they have today, the former having recently completed their Head Full of Dreams tour, reportedly grossing $523 million.

The live music scene in the UK is diverse, from small intimate gig venues to large scale arenas, stadia and festivals. Operated by global companies, this is a highly successful and competitive spectrum, but there are areas that need protection. Created in 2014, the Music Venue Trust is a registered charity to protect, secure and improve Grassroots Music Venues (GMV). There remains approximately 400 GMV in the UK, but some of the statistics are worrying. In 2007, there were 144 GMV in London, in 2016 there were 94, a 34.7% reduction in trading space. Of the 25 venues that helped launch Oasis' career in 1993, only twelve remain open. The reasons behind this can be attributed to repair and upkeep, rents and business rates, licensing and redevelopment, where landlords can potentially maximise value from the building. Concerns surrounding this were recently addressed by new planning policy.

On 24th July 2018, the Agent of Change principle was introduced as part of the National Planning Policy Framework. This seeks to provide protection to businesses and community facilities from newly granted planning consents. The principle states that existing businessand facilities should not have unreasonable restrictions placed on them as a result of development permitted after they were established. The responsibility to protect venues from issues such as licensing, trading hours and noise now lies with the developer.

To demonstrate why this was brought in:

Bristol, widely recognised as a city championing independent artists has reportedly lost 35% of its venues over the past decade. Planning changes introduced in 2013 that were designed to encourage more residential development by making change of use for buildings easier had the unintended effect of harming live music venues as developers brought forward schemes in traditionally non-residential, locations. Research in 2015 by Bucks New University, supported by UK Music, found 50% of dedicated music venues in Bristol were under threat from development, noise or planning issues. These included well-known venues such as Thekla, The Fleece and Fiddler's Club. The Agent of Change principle was introduced to protect such venues.

With pressures on smaller venues, larger operators encounter issues in securing sites and being able to deliver these. Whilst considering Bristol, one cannot ignore the ongoing saga of Bristol's long running arena project. Arguments to rectify the fact that Bristol remains one of the only major cities without a purpose built arena have been ongoing since 2003. It appeared a solution was found in 2015, when the city acquired an area of land more recently known as Temple Island, with the intention of building a 12,000 capacity arena. What followed was multimillion pound enabling works to facilitate this.

A change of Mayor led to a series of cost reviews calling the project into question, despite the investment and an experienced operator secured for the venue. Following the publication of a Value for Money report by KPMG, the Mayor announced in September that the arena would not be built on Temple Island. In parallel, a privately owned firm entered the debate promoting an arena at Filton Airfield, some five miles from the city centre, which they propose will be privately funded.

At the time of writing arguments continue, with new proposals emerging, but in my view not building an arena in the city centre is a missed opportunity. This would have a significant benefit to the surrounding businesses, whereas building an out of town arena threatens to undermine the city centre. One only needs to visit a city such as Cardiff to witness the vibrancy large music venues bring to a city and its economic and cultural scene. The additional benefits are significant, with smaller gigs being held in GMV when major artists visit and the buzz will be lost at an out of town site, lacking connectivity to Bristol's existing music scene. We have asked industry experts for their views on the UK live music scene:-

MARK DAVYD

What is your role/company?

I'm the CEO and founder of the Music Venue Trust, a registered charity which acts to protect, secure and improve grassroots music venues in the UK. I have been working in the live music industry for 36 years.

What changes have you witnessed in this time?

That's a small question with a massive answer. The entire structure of the music industry has changed, having massive impact on the sustainability and profitability of grassroots venues. One example is the removal of tour support budgets by major labels, a result of the downturn in business provoked by online piracy and streaming, which started in 2004. This had a huge impact on grassroots touring artists, which these venues have been asked to pick up. Subsequently, emerging artists are struggling to make tours work. That's just one example, there are dozens and dozens more - the explosion in upper level ticket prices and the complete standstill in grassroots ticket prices, I could go on for quite a long time.

What are the biggest threats facing the industry?

That, thinking about all the challenges, we sit still and hope someone else will sort it out for us. The outcome of that approach is that we continue to haemorrhage grassroots music venues at an alarming rate. If new artists don't have a stage they can walk on to for their first gig, we don't have future festival headliners. We need to align the whole music industry behind this basic concept. Every one of us has a stake in the success and sustainability of our grassroots music venues. We need to act on that stake, not permit those venues to fail through inaction.

What are you predictions for the industry going forwards?

That grassroots music venues will win. Because it is in these venues that the real enthusiasm and passion for music still beats strongest.

DAN ICKOWITZ-SEIDLER

What is your role/company?

Over 15 years ago I created Propaganda, the UK's biggest weekly club night. We occasionally feature live music at the event, and Ed Sheeran has even played. We also coown several live music venues with the promoters MJR. Our flagship and first venue was Tramshed in Cardiff, which launched in 2015 and has a 1,000 capacity as well as events space and a boutique cinema. Following its success we have purchased The Warehouse in Leeds, Plug in Sheffield, The Assembly in Leamington Spa and former Rainbow Warehouse in Birmingham, which we are reopening shortly as The Mill.

What changes have you witnessed in this time?

The growth of online music platforms and YouTube has had a positive impact on the live music industry. Never has there been such easy access to music. Subsequently, listeners are easily able to find new artists, which in turn means that artists are getting bigger quicker. With the widely-reported decline in music sales, live touring has become more crucial to artists and for many it has become their predominant income stream.

What are the biggest threats facing the industry?

With the continued growth of festival markets, bands and artists do not tend to tour in the summer. This makes the trade very seasonal for live music and consequently to be a successful live music venue it is crucial that you have a secondary income stream either through regular club events or having a multi-purpose venue space that can be used forweddings and private events over the summer.

What are you predictions for the industry going forwards?

People continue to crave live music experiences which can not be replicated online, I think we'll continue to see growth in the live music sector despite a challenging climate in some other areas of the entertainment industry.

GRAHAM WALTERS

What is your role/company?

I'm Chief Operating Officer of UK venues for Live Nation Entertainment and Academy Music Group Ltd. I have been working in the live music business for over 25 years now. Collectively, we own and operate 22 venues nationwide in 14 major cities, with capacities ranging from 250 up to 7,500. Many of our venues are of significant historical importance, some with Listed status and we have four prime sites in the capital, including the O2 Academy Brixton and O2 Shepherd's Bush Empire.

What are the biggest threats facing the industry?

Increasing rents is an issue, and it's also becoming more challenging to find suitable buildings. Licensing and planning laws are ever-changing, as is the rise of more city centre and residential housing nearby to live entertainment venues, a subject that has given rise to the Agent of Change Principle to protect music venues.

What are your predictions for the industry going forwards?

Music has never been more varied and musical trends evolve so much faster than they used to, which is partly down to streaming, digital services and social media. Bands play our much larger venues far more quickly than they would have say 10-20 years ago. Production values are now incredible, with limitless possibilities in staging, special effects, technical, sound, lighting and video.

As technology advances, there are far more opportunities to evolve in the live industry for sure, from how fans connect with artists, to developments we're seeing in Virtual Reality, but the passion for the live experience in-person will long continue. Digital advancements will also improve the ticketing systems further. Our partners at Ticketmaster are constantly working to improve technology to get tickets directly into the hands of fans.